The Most Important Determinant of Portfolio Returns

After decades of educating clients about the critical contribution asset allocation makes to long-term performance success, would it be heretical to suggest that there may be an even more important determinant of portfolio returns?

To view the full article please register below:

The Most Important Determinant of Portfolio Returns

In their seminal paper, “Determinants of Portfolio Performance,” authors Brinson, Hood and Beebower argued that investment policy was the largest determinant of portfolio returns, well ahead of market timing and stock selection.

In large consequence of this research, asset allocation became the foundation of investment advice to individual investors. After decades of educating clients about the critical contribution asset allocation makes to long-term performance success, would it be heretical to suggest that there may be an even more important determinant of portfolio returns?

Is Asset Allocation the Most Important Decision?

To ask the question is not meant to imply that asset allocation isn’t a cornerstone of the investment process. Nevertheless, it is an inescapable fact that equity investors continue to underperform the S&P 500 by a substantial margin.

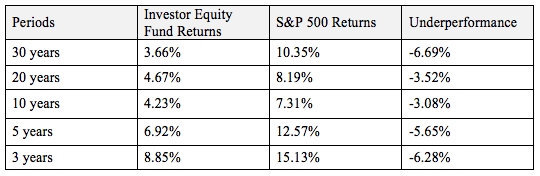

According to recent research, investor returns in equity funds have consistently underperformed the S&P 500 over both short-term and long-term periods, as evidenced by the chart below.

Investor Returns versus S&P 500 Returns

(as of Dec. 31, 2015)

Now, you might quibble a bit about the fact that the comparison of all domestic equity funds to the large cap S&P 500 is unfair, or that the index has no fees; however, the lag in investor returns, which are in hundreds of basis points, are impossible to dismiss.Source: http://www.talkmarkets.com/content/us-markets/dalbar-2016-yes-you-still-suck-at-investing-tips-for-advisors?post=96516

Investor Behavior Drives Portfolio Returns

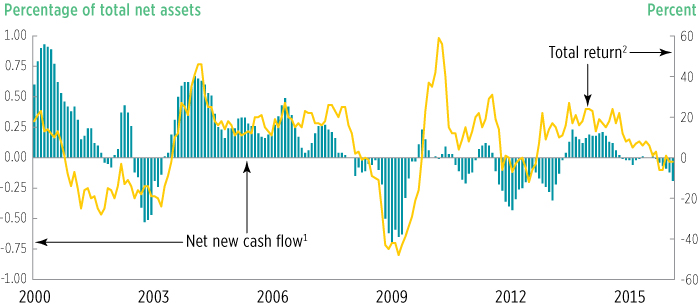

Having an asset allocation strategy is one thing. Sticking with it over full market cycles is an entirely different matter. As the chart below suggests, investor behavior commits the penultimate investment sin by buying high and selling low.

Net New Cash Flow to Equity Funds is Related to World Equity Returns

(Monthly, 2000–2015)

Source: http://www.icifactbook.org/ch2/16_fb_ch2

When net new cash flows into mutual funds are compared to equity returns, you see that investors tend to pull out of the markets as equity returns decline and add money after equity returns climb.

The inability of many individuals to stay invested during down markets or not chase returns during bull markets may, in fact, be more of a determinant of portfolio returns than any asset allocation decision.

Implications for Advisors

Behavioral finance continues to build a compelling body of research about how investor behaviors drive investment results.

Individual emotions and biases—such as fear and greed, herding and loss aversion—are behaviors that can undermine retirement plans and other accumulation goals.

For advisors, their most important value may have less to do with their portfolio management skills and more to do with how well they are able to manage their clients’ counterproductive behaviors. This is good news. Robo-advisors, for instance, may claim a superior investment platform, but they may never be able to argue that they are better than human advisors at managing the most important determinant of portfolio returns—investor behavior.

See referenced disclosure(s) (1) (2) at https://blog-dev.americanportfolios.com/disclosures/ .