FREE 11.1 Feature – Adam Mark

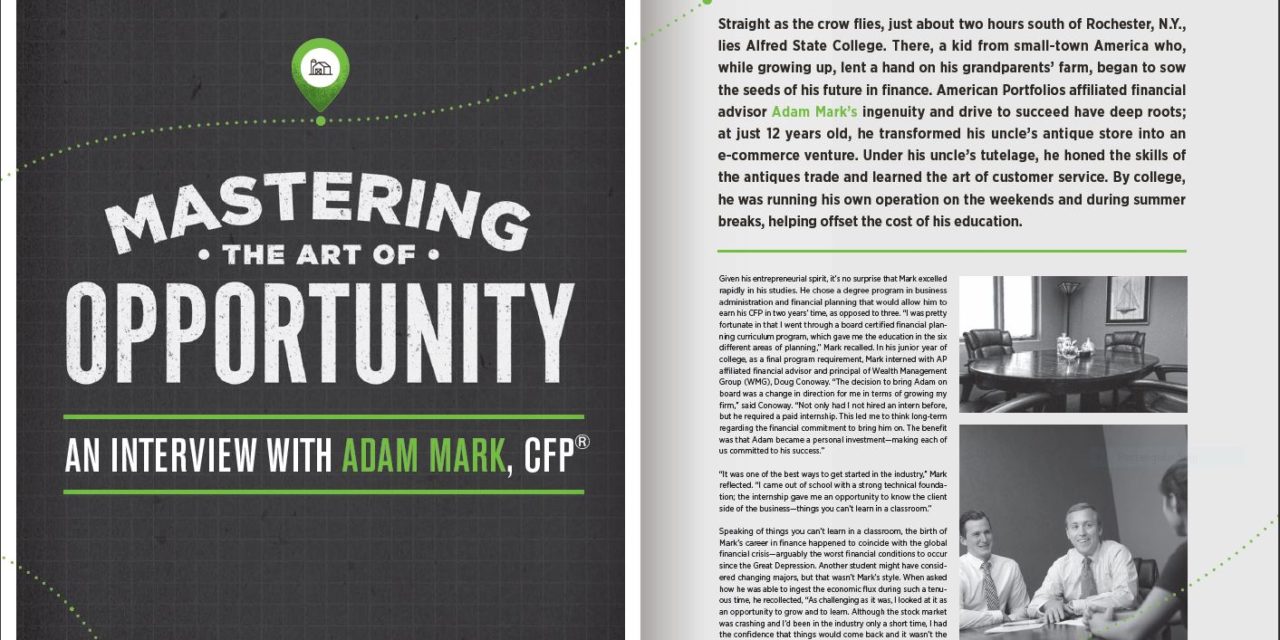

Straight as the crow flies, just about two hours south of Rochester, N.Y., lies Alfred State College. There, a kid from small-town America who, while growing up, lent a hand on his grandparents’ farm, began to sow the seeds of his future in finance. American Portfolios affiliated financial advisor Adam Mark’s ingenuity and drive to succeed have deep roots; at just 12 years old, he transformed his uncle’s antique store into an e-commerce venture. Under his uncle’s tutelage, he honed the skills of the antiques trade and learned the art of customer service. By college, he was running his own operation on the weekends and during summer breaks, helping offset the cost of his education.

To view the full article please register below:

FREE 11.1 Feature – Adam Mark

Mastering the art of opportunity

Straight as the crow flies, just about two hours south of Rochester, N.Y., lies Alfred State College. There, a kid from small-town America who, while growing up, lent a hand on his grandparents’ farm, began to sow the seeds of his future in finance. American Portfolios affiliated financial advisor Adam Mark’s ingenuity and drive to succeed have deep roots; at just 12 years old, he transformed his uncle’s antique store into an e-commerce venture. Under his uncle’s tutelage, he honed the skills of the antiques trade and learned the art of customer service. By college, he was running his own operation on the weekends and during summer breaks, helping offset the cost of his education.

Given his entrepreneurial spirit, it’s no surprise that Mark excelled rapidly in his studies. He chose a degree program in business administration and financial planning that would allow him to earn his CFP in two years’ time, as opposed to three. “I was pretty fortunate in that I went through a board certified financial planning curriculum program, which gave me the education in the six different areas of planning,” Mark recalled. In his junior year of college, as a final program requirement, Mark interned with AP affiliated financial advisor and principal of Wealth Management Group (WMG), Doug Conoway. “The decision to bring Adam on board was a change in direction for me in terms of growing my firm,” said Conoway. “Not only had I not hired an intern before, but he required a paid internship. This led me to think long-term regarding the financial commitment to bring him on. The benefit was that Adam became a personal investment—making each of us committed to his success.”

“It was one of the best ways to get started in the industry,” Mark reflected. “I came out of school with a strong technical foundation; the internship gave me an opportunity to know the client side of the business—things you can’t learn in a classroom.”

Speaking of things you can’t learn in a classroom, the birth of Mark’s career in finance happened to coincide with the global financial crisis—arguably the worst financial conditions to occur since the Great Depression. Another student might have considered changing majors, but that wasn’t Mark’s style. When asked how he was able to ingest the economic flux during such a tenuous time, he recollected, “As challenging as it was, I looked at it as an opportunity to grow and to learn. Although the stock market was crashing and I’d been in the industry only a short time, I had the confidence that things would come back and it wasn’t the end of the world.”

Having a veteran investment professional as a mentor helped Mark navigate the uncertainty of the future. “Being able to sit in on conversations Doug had with clients gave me the ability to see how they reacted. There’s a whole other side of the business that you have to be conscious of, and that’s the emotional side. I learned pretty quickly that sometimes the biggest value we add is to help clients transition through a difficult time. Those are the types of things you really can’t learn in school. And, there was no better time to learn but the present. As much as it was tumultuous and challenging, it was also the best time to get started in the industry.”

With the financial crisis raging full force, WMG would be tested to face yet another challenge. In July 2009, after their broker/dealer was bought out by LPL, it was announced they were rolling the B/D into the platform. It was at that moment that Conoway’s firm began evaluating other B/Ds, and American Portfolios quickly jumped to the top of their list. Mark attributes AP’s commitment to independence as a strong selling point. “At that point, we started to look at B/Ds that were willing to let us run the business the way we wanted to—specifically, accommodating our outside RIA to make sure we had flexibility. We wanted a firm that was big enough to have some ability to scale, but not so big that we would be just another number. AP seemed to be committed to independence, straightforward and had simple solutions that we were able to offer clients. We were not only able to make the decision to join AP, but we were able to make that transition happen all within a 60-day period.”

The initial relationship WMG forged with AP’s home office has blossomed since the practice’s 2009 affiliation. “It comes down to the team we’ve put in place around us and the people they rely on within AP. We’ve established a team that leans on the AP staff pretty heavily when we need assistance and have client requests,” Mark said of the relationship. “Without the team supporting me internally, I wouldn’t be able to do my job. They turn to AP to help them complete their job. We wouldn’t be successful as a practice without them.”

WMG’s ability to lean on AP continues to evolve within the uncertain landscape of the Department of Labor’s Fiduciary Rule. While the practice has always conducted about 60-70 percent of feebased business, AP’s advisory technology platform, Portfolio Insight, has been helpful. Mark attests that the technology has afforded them the ability to streamline and coordinate non-fee-based brokerage accounts with fee-based accounts. They define their strategy as a “core and satellite approach,” engaging the Nine Points Investment Model (NPIM) and strategic allocation portfolios as the core of many client portfolios. NPIM’s thirdparty manager platform helps them utilize “three distinct strategies within a client’s portfolio. The first satellite, a tactical equity strategy that offers additional return potential for a client focused on growth. The second is a core strategy that is typically a lower cost ETF-based portfolio. The third satellite is a tactical income strategy for clients who are a bit more conservative; it’s customized for every client based on the amount of risk they’re looking to take.”

From Mark’s perspective, technology is the hub that brings all the pieces of financial planning together. “Technology gives us the ability to become more efficient so we can spend time building stronger relationships with clients.” While some investors have been investigating the efficacy and cost differential of robo-advisors, Mark believes that this type of tool cannot replace the tangibility of the advisor-client relationship. “There are always going to be outliers, but I think the vast majority of clients appreciate an advisor who knows how to balance a use of high tech solutions with what’s most important to them personally.” The main concern is how this artificial relationship affects the client. “A robot can’t motivate a client to make the right decisions,” Mark observed. “They can use algorithms and a lot of different data, but they can’t build relationships.”

While the technical aspects of conducting feebased business are being addressed, so is the client conversation. Mark’s transparent approach not only educates clients, but puts them at ease. We’ve always structured the business in a way that clients understand the scope of our services and they know we’re being compensated on an ongoing basis through various investments. I think the critical part of our industry is always going to remain on the relationship with the client—and that has to be good no matter what.”

In fact, the client relationship is the core of WMG’s mission. They use a three-pronged approach to client retention and acquisition. They factor in marketing and networking to reach potential prospects, and have purchased Internet-based leads as a way to get a foot in the door. The main focus hones in on existing clientele and positioning that built-in trust into referrals so they can become a multi-generational firm. This approach, which begins with educating existing clients and confirming their investment plans, has proven to be mutually beneficial. Encouraging clients to educate generations of their family organically leads to referrals. By getting to know their clients’ children, they’re able to discuss aspects of financial planning that, in many cases, might be left unaddressed. By enlightening referrals, they can plan for complexities, such as long-term care, asset protection and inheritance. “Many of our clients listen astutely as we talk to them about the fact that mom and dad’s money may be at risk, and their potential inheritance could evaporate if they don’t step in.”

Much like an individual, a practice also plans for the future. For Conoway, that plan relies upon his partner, Mark. In the time that Mark has been with WMG, he has risen to become the natural successor. The groundwork of the succession plan was laid about six years ago—fairly early in his tenure. They are now in the home stretch of the planning phase where a vast majority of the ongoing shift to advisory of their individual client relationships have already transitioned. At some point in the near future, Conoway’s role will shift to advisor emeritus status. “My original commitment to Adam was if the internship worked out, I’d make him an advisor; and if that worked out, I’d make him a partner,” Conoway recalled. “Eight years later, here we are! I think it has turned out extremely well for both of us, and I’m fully confident my clients will be exceptionally well-cared for in the future, when I step back.”

When asked what advice he has for advisors who haven’t developed a continuity or succession plan, Mark suggests, “Start sooner rather than later. It’s as simple as having conversations about your firm’s continuity plan to answer the questions: What if you can’t work tomorrow? Do you have somebody that can step in? If so, great; have the conversation, put something in writing and let your clients know. If you don’t have anyone lined up, start looking for advisors within the same B/D or the professional financial services organizations you feel could be a good fit.” True to form, Mark is always looking ahead. “In order for our firm to be sustainable, we have internal candidates that we’re training; younger advisors coming up that hopefully will become part of the practice and partnership someday. While that’s happening, I’m also having conversations with other like-minded advisors looking for their own continuity or succession plan. It’s important for my own continuity, but I may also be able to step in and help them.”

As a younger-than-average advisor, Mark understands how important networking is to success. While his age has called his experience into question on the rare occasion, he says he’s more frequently experienced the opposite. “I think the opportunity for any young advisor is when people are retiring especially, and they’re a little bit older. They want to hire the advisor that’s going to be their advisor for the rest of their lives. Also, when it comes to multigenerational planning, they see the opportunity for me to continue working with their heirs even after they are gone.” The best advice Mark received prior to starting his career was to be patient and give it time. “It’s not an easy road establishing yourself as a younger advisor; definitely, there is a reward at the end.”

Part of that reward is sharing his knowledge and experience with CFP students at his alma mater and serving on the local Society of Financial Services Professionals board. His focus is to help young advisors break into the business. He admits that there is a “need to be serious about our profession and the future of the industry.” The aim is to train young financial advisors “the right way and make sure opportunities are going to exist, the same way they existed 30, 40 years ago.” For Mark, making the most of opportunities is the key to his success and what will continue to serve him throughout his career. While others may pass up opportunities, he seizes them with ingenuity, drive and ambition. Looking ahead, he sees one of his goals as helping to “grow and build a team of next-generation advisors; that we can work together with the common goal of serving our clients so they have peace of mind and can accomplish their dreams.”

Dreams also include personal goals. In addition to financial planning, Mark is in the midst of family planning. In July, he and his wife (and their two rescue puppies) will welcome a daughter into their growing family. When asked about his thoughts on becoming a father, Mark ponders, “I think it’s going to be a whole new world.” If the past is any indication of the future, his “whole new world” will be a wonderfully successful one.